Table of Content

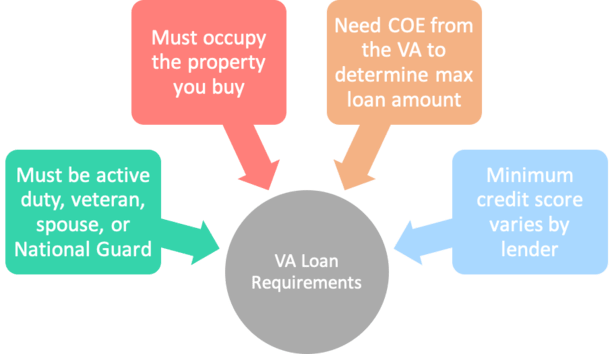

Companies displayed may pay us to be Authorized or when you click a link, call a number or fill a form on our site. Our content is intended to be used for general information purposes only. It is very important to do your own analysis before making any investment based on your own personal circumstances and consult with your own investment, financial, tax and legal advisers. For example, if you put five percent or ten percent down on your VA mortgage, your VA loan funding fee is reduced depending on which amount you pay. Lenders may have a maximum allowable threshold for derogatory credit, which can include collection debt. The VA guidelines state that they will consider a borrower still paying on a Chapter 13 Bankruptcy if the payments to the court have been satisfactorily made and verified for one year.

If your credit score isn't quite up to par to qualify, the first thing you should do is get a handle on what your score is and what's on your credit report. You can get your free credit score and report from Rocket HomesSM 1 once a week. This will give you your free VantageScore® 3.0 credit score and report courtesy of TransUnion® monthly. The VA has very specific guidelines not only for a client’s personal financial qualifications, but also for the property itself.

Where to Get Credit Resources?

In 2004, only two percent of all active mortgages were financed via the VA housing program. In 2012, 1.5 million veterans maintained mortgages, which had been secured with VA insured financing. As a result of an estimated one-million active duty service-members being discharged within the next five years, it is believed that loan usage will continue to expand. The coverage against loss is good for the lenders but they are still not covered 100%. They are also in the business of making money and if the borrower is not making the mortgage payments, then the lender still has some risk. It is for this reason why lenders have their own credit score minimums.

Lenders may also a debt to income ratio requirements even though VA does not have a maximum DTI Cap due to their own lender overlays. VA has one of the most lenient credit requirements out of all mortgage loan programs. Explore bad credit home loans – If you’re a first-time homebuyer or otherwise qualify for low-income loan programs; you have options beyond a conventional loan. VA loans and USDA loans have no down payment requirement and no set credit score requirement, so ask your lender whether you’re eligible. The Fannie Mae HomeReady and Freddie Mac HomeOne and Home Possible loan programs are worth exploring; too, along with many first-time homebuyer programs.

VA Funding Fee Requirement For All VA Mortgages

Two big advantages of VA loans are competitive interest rates and no down payment requirements. You’ll often hear these additional requirements called “overlays.” A credit score requirement is among the most common. We do our best to partner with VA lenders who allow for lower credit scores without many overlays. Lender guidelines are changing constantly and the lenders referenced above are just a small sampling and may not be the best option for you.

The VA loan program seeks to accommodate as many military buyers as possible with a simple and accessible mortgage. Regardless of the loan you’re seeking, you’ll typically need to meet a lender’s minimum credit score to secure financing. These cutoffs vary from a lender, loan type, and specific financial situation. If a borrower has sufficient residual income, some lenders will even approve VA loans with credit scores as low as 500. Typically, lenders use a process known as automated underwriting when they review your VA loan application.

Manage Your Mortgage

The company name, Guaranteed Rate, should not suggest to a consumer that Guaranteed Rate provides an interest rate guaranteed prior to an interest lock. Answer a few questions below to speak with a specialist about what your military service has earned you. The borrower needs to get approve/eligible per Automated Underwriting System. Just home buyers are Veterans of the United States Armed Forces with a Certificate of Eligibility does not automatically guarantee them a VA Loan. Borrowers can also qualify for VA Loans With Low Credit Scores.

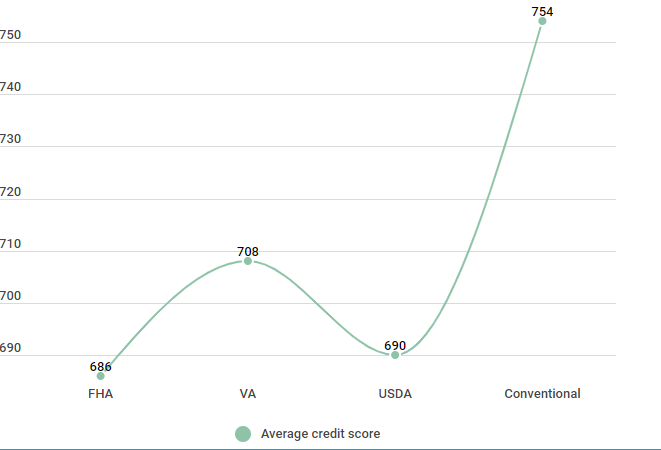

For example, applicants for the FHA loan must have at least 580 to qualify, unless the borrower wants to put down a larger down payment. Regardless of their disability rating, disabled veterans with VA loan eligibility are qualified for a VA home loan if they fulfill the requirements for the loan. While standards differ, veterans generally must meet minimum service criteria, have a good credit score, satisfy the minimum income limits, and possess an acceptable debt-to-income ratio. The debt-to-income ratio is the minimum mortgage payments on all your debts divided by your gross monthly income before taxes are taken out, without factoring in any other debts. Options include no or low down payments, lower closing costs and interest rates, and no mortgage insurance costs. There may also be more flexible VA loan credit score requirements.

Current Mortgage Rates for Varied Credit Scores

If you’re not sure what your credit score is, you can check it for free on websites like Credit Karma or AnnualCreditReport.com. Once you know your credit score, you can start shopping around for lenders that offer VA loans to borrowers with your credit profile. Lenders consider other factors, as well, including loan-to-value and debt-to-incomeratios, but credit scores are especially important. Understanding what an adequate credit score is an excellent starting point for anyone trying to secure a VA loan. A credit score is one factor a lender looks at when determining mortgage rates. The score allows them to project the risk they are taking by lending money to an individual.

Regardless of the type of loan you’re seeking, you’ll typically need to meet a lender’s minimum credit score in order to secure home financing. These cutoffs can vary depending on the lender, the loan type and your specific financial situation. Unfortunately, there’s no easy way of knowing what credit requirements you need to meet. You need to speak to various lenders to choose the best course of action for you and see who will offer you the best interest rate.

It’s the role of underwriting to make sure that a borrower meets a lender's guidelines. This includes ensuring qualification from a credit perspective. In the next couple of sections, we’ll also introduce a couple of terms you may not be familiar with. The use of compensating factors is an accepted industry practice. Borrowers who make down payments on VA mortgages should know that there are definite benefits to doing so even if you are forced to because of lower FICO scores. Credit scores affect multiple parts of your home loan, not just the approve/deny factor.

When applying for a new credit card, mortgage or any other loan, you will experience a hard inquiry which actually damages your credit score. In addition, the court trustee will need to give written approval to proceed. Expect your lender to require a full explanation of the bankruptcy. The borrower must also have re-established good credit, qualify financially and have good job stability.

The VA doesn’t issue loans and doesn’t set a credit score requirement, but their lenders typically do. So potential borrowers don’t have to be blemish-free or have elite credit scores to secure VA financing. Lenders set their credit score requirements, which vary from one lender to another. However, most lenders require a minimum of a 640 credit score. As mentioned above, the VA itself does not have a set minimum credit score requirement, but they do trust private lenders to properly vet the borrower to understand their financial stability. The VA’s role in the loan process is to fund and manage the program and be sure it runs smoothly; they do not issue the loans themselves, that is left to the mortgage lenders.

Guaranteed Rate, however, will accept scores as low as 580 if the loan amount is under $647,200. They will accept a score of 600 for loan amounts under $970,800, and anything above that, a 620 as the lowest score. Lender requirements have relaxed, and the average credit score for FHA loan in 2021 landed 672, which is still relatively high compared to the pre-pandemic average of 665 in 2019. A disabled veteran who receives compensation from the VA for a service-connected disability, for example, is exempt. Keep in mind that your score can vary between the three credit reporting bureaus, Equifax, Experian and TransUnion. Most lenders look at the middle credit score of the three when considering you for a mortgage.

Another option is to find a cosigner who has a strong credit history. This can help you get approved for a loan, but it’s important to remember that you’ll be responsible for repaying the entire loan, even if your cosigner is making the payments. But the VA also doesn’t make these loans, and they’re made by banks and lenders like Veterans United, which will almost always have a minimum credit score that buyers need to qualify. When it comes to getting a VA loan, there actually isn’t a definite minimum credit score that’s required, as different lenders will have their own criteria. That being said, a credit score of 580 is considered to be a good benchmark to have when applying for a VA loan.

The larger and most recognizable lenders in the industry do not accept lower credit scores. We will outline a few of those below and will describe what their credit requirements are. USDA loans are yet another government-backed option, but they're only available in rural areas. The USDA does not enforce a minimum credit score, but like other government-backed options, most USDA lenders are looking for a score in the mid 600s. Remember, if you do have a low credit score, there are still options available to you. One option is to get what’s called a “manual underwrite.” This means that a human will review your application instead of relying solely on your credit score.